Your Money Is Fake (The Money Printing Mechanism & How To Protect Yourself)

You're powerless without financial literacy. Learn to identify how your money is being printed out of thin air and position yourself to benefit.

There are some days you never forget.

I’ll always remember where I was when I learned how money really works.

Four years ago, in October of 2020, I was sitting at my desk reading an article just like this one.

“They print it out of thin air.“

At first, it sounded like a conspiracy theory.

But the deeper I dug, the more I became captivated — the more I understood.

Topics I couldn’t explain before suddenly became crystallized for me:

why the cost of living continues to skyrocket

why investments go “up“ in value

why our government seemingly always has excess money to spend

The answer?

Money printing.

One thing’s certain: my discovery of these drivers was timely.

At the time, we were in the midst of a remarkable rebound from the infamous Covid-19 stock market crash.

The catalyst for the turnaround?

Well, money printing.

The US Federal Reserve “printed” $5 trillion of new money to stimulate the economy.

The result?

The influx of new money into the economy caused the price of everything to be bid up sky-high, creating a perfect V-shape recovery back to pre-pandemic stock prices.

But my research on money printing made one thing clear:

We were going to achieve much more than just parity.

From pre-pandemic levels:

Stock market indices ripped by 30%

Real estate in desirable locations saw gains of 30%

Bitcoin saw a 17x return from the lows of the crash

Despite the world being no better off than before the pandemic, the rich got richer.

And new millionaires were minted too:

Yeah — 5.2 million of them, to be exact.

So here’s the question:

If you weren’t one of them, why didn’t you capitalize?

Why didn’t you see it coming?

You didn’t know what to look for.

You sold your assets during the turmoil of the pandemic, only to see them skyrocket in value within the span of a few months.

Your purchase power took a nosedive — losing 30% of its value at the snap of the Fed’s finger.

You missed the biggest buy signal ever issued due to a lack of financial education.

If you understood the mechanism behind money printing, you could have front-run the market and secured your financial freedom.

My goal with this newsletter?

To teach you:

how money is printed

track the growth of the money supply yourself

position yourself to benefit from it

Let’s get right into it.

Decoding The Monetary Cipher

Here’s the thing — they don’t call it “money printing” on its face.

Central bankers rely on complex jargon to obfuscate an otherwise simple procedure: increasing the money supply.

To understand what’s going on, you need to understand the language of finance.

Think of it like a cipher.

A cipher is a method used to encrypt information.

If you’re unaware of the proper method to decode it, you’ll be unable to convert the cipher into anything more meaningful — it will look like gibberish.

If you don’t have an understanding of…

the language of central bankers

the mechanism of money printing itself

…you won’t grasp the underlying signal.

Or even worse, be tricked into thinking it isn’t happening.

If you’re going to take anything away from this article: think for yourself.

Don’t take what financial newspapers and economists say at face value.

Why do I say this?

Let’s take a trip back to 2020.

When the Federal Reserve announced it would begin increasing the money supply to stimulate the pandemic economy, news outlets first parroted the narrative that the expansion wouldn’t lead to inflation.

Newsflash: they were wrong — and the people who knew it were banging the drums.

On top of being vocal, market participants who actually understood what was about to happen put their money where their mouth was.

They chose to position themselves in assets that would benefit from inflation, knowing that it was inevitably coming.

When it became impossible to ignore that inflation was beginning to manifest itself, the Federal Reserve was forced to finally acknowledge it.

But they brushed it off, stating that the inflation would be temporary and short-lived.

Again, the central bankers in charge of our financial system were either wrong or malicious — you choose which one to believe.

According to the Bureau of Labor Statistics, consumer prices are still 21.2% higher than they were pre-pandemic as measured by Consumer Price Index (CPI).

And I’ll give you a hint: they’re never coming back down.

Even still, the CPI fails to reflect the true rate of inflation — it’s much higher than the government wants you to believe.

To learn how the government manipulates the CPI metric and the motivation behind it, check out my newsletter below:

Here’s the bottom line:

Trust no one.

The onus is on you to protect your purchasing power.

Now that you know financial literacy is needed to decode the Federal Reserve’s actions, let’s get into how “money printing” actually works.

The Money Printing Mechanism

Yes, the Federal Reserve technically does print physical cash.

But here’s the thing:

The $5 trillion introduced to the economy during the pandemic wasn’t physical.

When we talk about “money printing,” it’s not as simple as firing up the printing press.

To understand how new money is injected into the economy, you first need to understand how US government treasury bonds work:

Treasury Bonds

Okay, let’s keep this simple.

US Treasury Bonds are essentially IOUs from the government.

Individuals, companies, and even foreign governments want to earn a yield on their cash balances.

So what do they do?

They lend their money to the US government, which is offering to pay them interest on their cash balances.

But you might be asking:

What does the government get out of this?

Why would the government be willing to pay interest for access to their money?

Here’s why:

The US government spends more than it collects in taxes — they operate in a deficit.

This means they need to issue debt (bonds) to entice people to front the cash needed to meet the government’s operational expenses.

As we already went over, many entities are willing to buy these bonds for the yield that they provide.

But until now, we’ve left out a major buyer: The Federal Reserve.

The Federal Reserve: The Buyer Of Last Resort

Now, let’s talk about the big player — the Federal Reserve.

Let’s say that the government needs to finance a massive amount of spending.

For example:

$1.5 trillion — bailing out the banks that were a part of the 2008 financial crisis

$5 trillion — economic stimulus in response to the Covid-19 pandemic

If the government can’t raise the money from existing bond buyers, the Federal Reserve will customarily step in as the buyer of last resort.

The Fed has the power to “create” money, enabling them to buy as many bonds as needed for the US government to fund their objectives.

Here’s how it works:

The Fed announces its plan to buy U.S. Treasury Bonds (and other securities like mortgage-backed securities)

Big banks buy the bonds on the open market and then sell them to the Fed.

In exchange, the Fed credits the banks with newly “printed“ money

With the stroke of a few keys on a computer, the Federal Reserve just created new money out of thin air.

So, how does this newly created money cause inflation in the broader economy?

When the Fed credits the new money to the banks in exchange for government bonds, their bank reserves are increased, giving them a greater capacity to lend money to businesses, consumers, and other financial institutions.

Money & credit that didn’t exist before are now part of the system, causing inflation — the money supply has expanded.

Tracking Money Supply Expansion

Okay, now that you know how the Federal Reserve adds liquidity to the system, you might be wondering:

How can you measure the amount of money added to the system?

We can quantify this through what are known as monetary aggregates:

M0: The Monetary Base

The M0 money supply is the physical cash in circulation plus bank reserves.

Think of this as the hard cash in people’s hands and bank vaults.

M0 reached an inflection point in response to the 2008 financial crises and, more recently, the Covid-19 pandemic stimulus.

Currently, we have about $5.67 trillion of physical cash + bank reserves in circulation.

M1: Liquid Bank Deposits

M1 Money Supply includes everything in M0, but it also adds liquid bank deposits.

This is the money sitting in checking accounts and savings accounts, ready to be withdrawn at any time.

In other words, it’s money that’s easily accessible — cash in hand or a swipe away on your debit card.

See that massive spike in 2020?

I’ll let you guess what happened around that time:

Money printing.

We went from around $4 trillion to $16 trillion in the blink of an eye, eventually increasing even further to the current figure of $18.1 trillion.

M2: Savings

The M2 money supply metric includes all of M1, but adds money market savings accounts, certificates of deposit (CDs), and other types of savings.

M2 is the money supply metric that’s most useful to you when benchmarking your investments against monetary inflation (more on this later on.)

It’s a wider view of the money supply, representing not just the cash in circulation but the near-cash equivalents sitting in your savings accounts.

This money isn’t as liquid, but it’s still part of the overall money supply.

Our M2 money supply currently sits at $21.1 trillion in circulation.

Using Money Supply Metrics To Your Advantage

Now, you might be wondering:

How can I use these money supply metrics to my benefit?

These metrics are invaluable due to their correlation to financial markets.

Let me explain:

In the following chart, you can see that the amount of securities (bonds) held by the Federal Reserve is directly correlated to the M2 money supply.

In other words, the amount of securities they’ve purchased dictates the amount of money in circulation.

This lines up perfectly with what you’ve already learned: not exactly a shocker.

But here’s what you might not already know:

When you dig deeper, you’ll find that the vast majority of the movement in asset prices occurs in tandem with the M2 money supply.

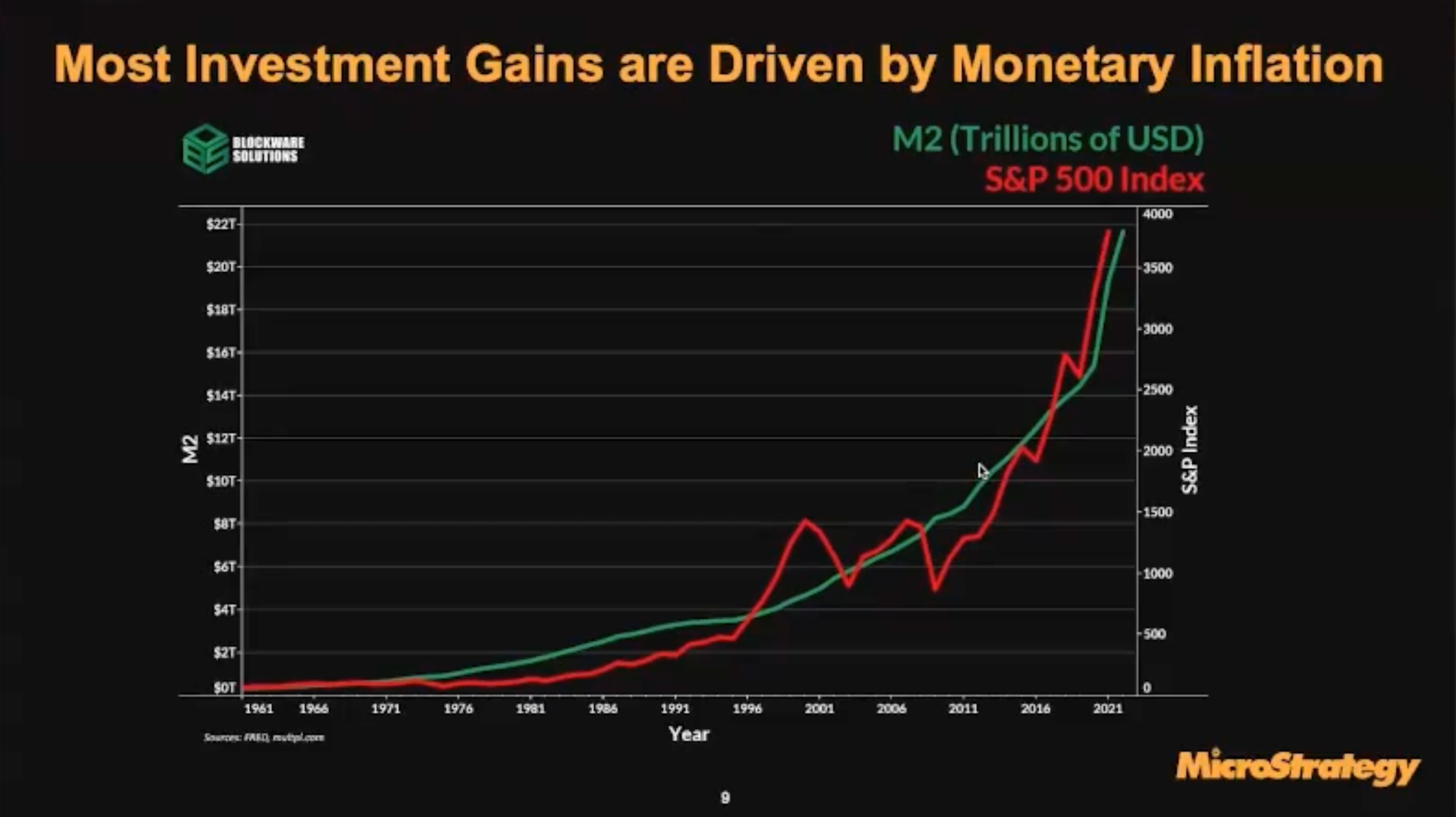

Here’s a chart (borrowed from MicroStrategy) showing how the S&P500 stock index (an index of the 500 most valuable companies in the US) moves relative to the M2 money supply:

Spoiler alert: the movements are virtually identical.

When money supply goes up, asset prices go up.

Now, let’s get to the heart of this.

What does knowledge of these relationships enable us to do?

With these metrics in your toolbox, you can predict asset inflation with certainty.

Let’s again look at the Covid-19 pandemic as an example:

In March of 2020, the S&P500 crashed to the tune of a 37% drop.

But if you knew what to look for, the widespread panic was an obvious opportunity.

As the market plummeted, the Fed announced its intention to purchase trillions of dollars of securities (thereby injecting liquidity into the market).

As a result of the purchase, the M2 money supply began to skyrocket — at the exact same time that the stock market was having a meltdown (you can see this disparity on the above chart).

The result of the stimulus?

The market didn’t just rebound — asset prices across the board went up by 30% above prior highs (the same % increase as the money supply).

I don’t know how else to say it: this isn’t a coincidence.

Let’s look at this dynamic over the long term for good measure.

Here’s a chart displaying:

M2 Money Supply

Net Worth Held By The Top 0.1%

Net Worth Held By The Bottom 50%

What do you see?

The net worth of the top 0.1% tracks the increase in the money supply perfectly, while the bottom 50% hardly see their wealth increase by comparison.

But why?

What do wealthy people own that poor people don’t?

Assets that keep up with the monetary inflation rate.

The ultra-wealthy understand the game that’s being played.

To understand the game and how the wealthy combat inflation through their investment vehicles, this newsletter is a good place to go:

Staying Ahead Of The Money Printer

Let’s face it:

The money supply rarely ever contracts — and if it does, it’s very short-lived.

The writing is on the wall.

The Federal Reserve is going to continue to print money at the behest of the US government as long as the dollar system exists.

But now you have an edge.

You can use your knowledge of how money is created to your advantage.

Here are some actionable steps you can take that will keep you ahead of the curve:

Monitor Economic Indicators: Keep an eye on the news headlines and key data like M2 money supply, but don’t take what they say at face value. Sift through the noise to develop the conviction in your positions needed to double down during market crashes.

Use A Proper Hurdle Rate: Use the rate of expansion of the M2 money supply as the hurdle rate on your investments. If the money supply grew by 10% in a given year, but your investments only returned 7%, you lost 3% in purchasing power.

Buy & Hold Assets: Buy scarce and desirable assets that will keep up with the rate of monetary expansion and hold them over the long term to defend the purchasing power of your dollars.

Stay informed, stay prepared, and always keep an eye on the money supply.

Until next time.

— Landon

*The content of this article is for informational purposes only and does not constitute financial advice. Do your own research before making any investment decisions.

Love it!!!