You're Being Stolen From Every Day (How To Build Wealth In A Broken System)

Inflation is cutting the value of your money in half every 10 years. What are you doing to protect it?

I'm going to tell you something you probably already know deep down:

The system is rigged.

Look around you.

The prices for housing, healthcare, quality food, and formal education are skyrocketing.

Every passing day, the building blocks needed to lead a good life are moving further and further from your reach.

No matter how much you save, it seems like you just can't get ahead.

A shocking 63% of WORKING Americans have already been pushed to the brink of financial ruin — they can't even afford a $500 emergency expense.

I hate to be the bearer of bad news.

But things are only going to get worse for the average person.

How do I know this?

After hundreds, perhaps even thousands of hours of studying, I know that this problem is systemic.

Once you have this understanding, it should be no surprise that despite the poor and middle class suffering, the richest among us have never been doing better.

Lamborghini just sold 10,000 cars for the first time in it's history.

So how can the wealthy create such a large divide between themselves and the average person?

Because THEY know how the system works.

A lack of financial education is the greatest cost to your livelihood you will ever endure.

The average person will spend a third of their entire life focused on bringing home the next paycheck.

40 hours a week x 52 weeks x 40 years = 90,000 hours.

But they won't devote a few hours to understand how to retain the value they have already earned.

They'll never understand that their savings, productivity, and time are being stolen from them.

Wake up.

Through education, you can understand the rules of the game.

And you'll be able to play like the wealthy play.

Let me show you how.

What Is Inflation?

Unless you've been living under a rock, you've likely at least heard of inflation.

Everyone experiences it's effects when purchasing just about anything.

It's the subject of conversation everywhere from economic forums, to cable news, to major newspapers, and even on X (formerly known as Twitter).

Financial markets move violently based what the inflation rate is reported to be.

And your education on the subject determines if you benefit or suffer from it.

But what actually is it?

To explain inflation, I offer you my personal experience with it:

My family first started the Dal Rae Restaurant 73 years ago.

Since it's establishment in 1951, it's distinguished itself as one of the best steakhouses in the Los Angeles area.

We’ve prided ourselves with preserving the restaurant's original atmosphere to a tee.

Everything from the dimly lit leather booths to the table side service remains frozen in time.

Our longest-tenured customers bring their grandchildren in to dine on the same food they did as kids.

But there is one thing that was unable to stand the test of time: the menu prices.

When the Dal Rae first opened, we served our 16oz New York steak for $3.95.

Today, we are forced to charge $68 to earn the same margin.

Over the course of 73 years, our steaks have gotten 17x more expensive.

But what's driving this?

Is cattle more scarce than it was back then?

Nope, we have roughly twice the amount of cattle to source from in the present day as we did in 1951.

Are we price gouging and taking advantage of our customers, without whom we would lose our family livelihood?

Nope, we maintain the same profit margin on our steaks since we first opened.

The culprit is inflation.

Inflation is an increase in the total money supply.

Under the current fiat monetary system, governments have the ability to expand the money supply at will by "printing" new dollars.

Here's a simplistic example:

Assume all of the money in the world adds up to $100 million (it doesn’t, but stay with me here).

If I bring another $10 million into circulation out of thin air and give it to my friends, we would move the total supply from $100 million -> $110 million.

Thus, the inflation rate would be equal to the 10% increase in the money supply.

This manipulation of the money supply has cascading effects throughout the entire economy.

The price increases you see in goods, services, and assets are a symptom of inflation.

The reason for this comes down to the basic principles of supply and demand.

In other words, if you:

Hold the amount of goods, services, and assets in the economy constant

Increase the supply of currency in the economy

More money (higher demand) will be chasing the same amount of stuff (stagnant supply).

Price increases will ensue as market participants bid up prices in competition with each other to secure limited resources for themselves.

In effect, the end result is the currency has become less valuable — it's been debased.

However, the price increases that result from inflation don't manifest themselves equally in all goods and services.

As billionaire Michael Saylor puts it, inflation is a vector.

What does this mean?

Think of it this way:

The price of everything is constantly varying everywhere all the time.

When we observe pricing trends in the market, it's obvious to us that the cost of a loaf of bread isn't going up as fast as real estate prices in Newport Beach, California.

But why?

The main drivers are scarcity & desirability.

When the prices of goods rise due to increased demand, manufacturers of those goods are incentivized to further increase the supply of the good to satisfy the consumer.

The more easily the supply of a good can be increased, the less the good will go up in price, even in the face of massive inflation.

This is why most highly industrialized foods and things like internet streaming services tend to show little price appreciation overall.

However, assets that are scarce and hard to create more of tend to be the most respondent to inflation.

For example, no matter how hard you try, you'll never be able to recreate another Mona Lisa — it's a one-of-one work of art.

As a result, the price of the original will keep pace with the true inflation rate, because demand for ownership of this historical artifact cannot be satisfied by increasing the supply of the asset.

An understanding of this aspect of inflation is critical to understanding the philosophy the rich use to preserve their wealth across generations.

Now if you've had any prior education in finance, you might take issue with something I've implied above:

The traditional investment community believes that the returns from these assets tends to outperform inflation by a wide margin.

For example, assume the S&P 500 stock index has an average year, returning 7% on your investment.

If the inflation rate reported by the government is 2%, traditional investment advisors would think that you've made 5% real returns.

Sadly, this is completely untrue — yet it is continuously taught at the highest levels of education.

The reason?

The government-issued inflation number provably understates inflation.

This means that, contrary to popular belief, your real returns are 0%.

Or much, much smaller than you think.

I'll have a separate newsletter coming out soon that explains why this is the case.

Saving Is For Losers

Here's the truth:

The government has destroyed the ability for people to save in dollars over the long term.

Saving for your retirement in a bank account simply isn't a viable strategy anymore.

The advice your grandmother gave to you no longer works.

The game has changed.

Inflation is designed to steal your purchasing power.

Let's assume my grandfather decided save his profits from the restaurant in a bank account earning him 0% interest on his money.

Colloquially, you might call it stuffing it under the mattress.

Over the course of the last 73 years, for every dollar he made off of the New York steak he sold in the restaurant's early days, he would have suffered a 95% decline in his purchasing power.

How is this possible?

Due to inflation, prices for goods, services and assets rose all around him.

But the number of dollars he has in the bank isn’t growing — he’s getting poorer.

Essentially, the government stole 95% of the value he provided to society and redistributed it to the beneficiaries of the newly printed money.

The most sickening aspect of it: it's almost like he never even contributed in the first place.

But he wasn’t the only person to lose value:

every employee he ever gave a livelihood to

every supplier he ever paid for goods

every customer who he could have ever served

They would have all had their wealth stolen in the same fashion.

Now let’s work with real numbers:

Let’s assume you had $10,000 saved in a bank earning 0% interest for 20 years.

We’ll also assume that the inflation rate over that period of time is 2% every year (the government’s yearly inflation target).

At this rate of currency debasement, at the end of the 20 years, your $10,000 savings account would only be worth what approximately $6,729.71 is worth today.

Your purchasing power would decline by an astonishing 32.7% over the span of 20 years.

But sadly, this steep loss in purchasing power doesn’t even come close to portraying the reality of the world.

Economists that don’t subscribe to the government’s inflation measure, like Saifedean Ammous, have concluded that the real inflation rate for scarce and highly desirable assets averages at 7% per year.

This means that over 20 years, your $10,000 would only be worth what $2,584.19 is worth today.

A staggering 74.1% decrease in purchasing power.

In just 10 years, your purchasing power would be cut in half.

Don't believe me?

In January of 2004, the S&P 500 stock index was 1,131.

At time on writing, the index is 5,350.

If you chose to wait until today to buy this basket of stocks, you can now buy 78% less than you could have 20 years ago.

Keep in mind: there may be cases where the prices of certain goods actually falls falling DESPITE inflation due to technological innovation or other factors.

Even still, the effects of inflation over the last 70 years of innovation have been so pernicious that even some of the highest earners in our society are unable to keep up.

Just 7% of US households make $250k per year.

Yet, the cost of living is so high that a third of these households are living paycheck to paycheck!

In other words, they aren't saving ANY money for their future retirement.

Here's what's even more shocking: they probably wouldn't even be able to retire through saving if they tried.

Over 7 in 10 investors believe that the required savings for Gen Z and Millennials to retire comfortably is now in the ballpark of $3 million to $5 million due to inflation.

Let's assume you're earning $250k per year — setting aside that this alone is a dream for most.

After you pay your 50% in taxes, your true take-home is about $125k a year.

As far as their budgeting of that money goes, we'll give them the benefit of the doubt.

We'll assume the person is at least semi-responsible with their money and following the popular 50/30/20 rule:

50% of your income on obligations — rent, car payment, groceries, etc. ($62.5k)

30% of your income on discretionary spending — what you want, but don't need ($37.5k)

20% of your income on savings — emergency fund, debt repayment ($25k)

At the end of the day, this budgeting strategy would leave you with $25k a year to save.

But at this rate of savings, it would take you 120 years to hit your $3 million dollar retirement target.

Screw it.

Let's assume you live as frugally as humanly possible, reduce your discretionary spending to ZERO, and save $62.5k per year (half your after-tax income):

It would still take you roughly 48 years of nonstop saving to achieve retirement.

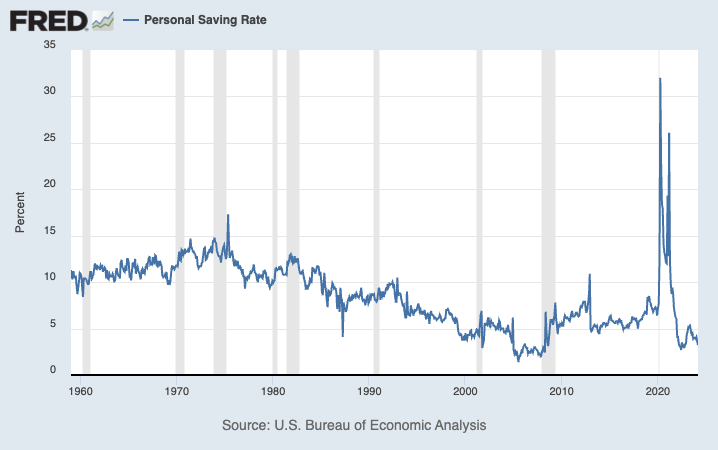

And just to be clear, the average personal savings rate is nowhere near 50%.

Or even 20%.

At time of writing, the average personal savings rate is just 3.2%.

But yes, there is a caveat to this.

Inflation will also cause your wages to increase over time.

But there's a problem.

Historically, wage increases haven't kept up with inflation.

Unfortunately, most labor isn't as scarce as the assets you seek to buy with the fruits of your labor.

As a result, your wage increases will likely never keep up with the increase in the price of the assets you are seeking to buy.

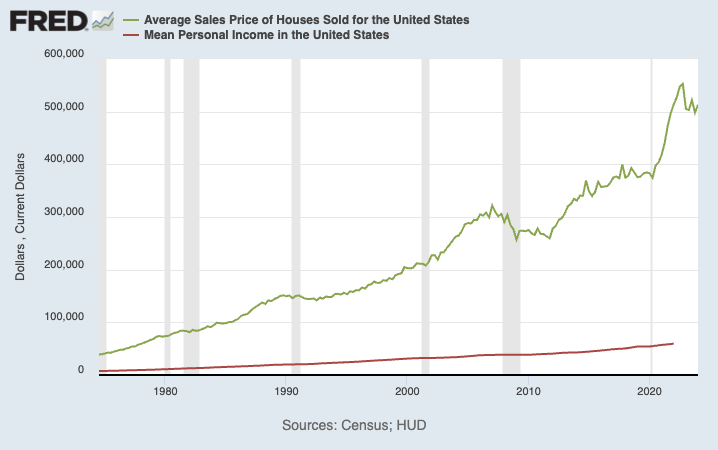

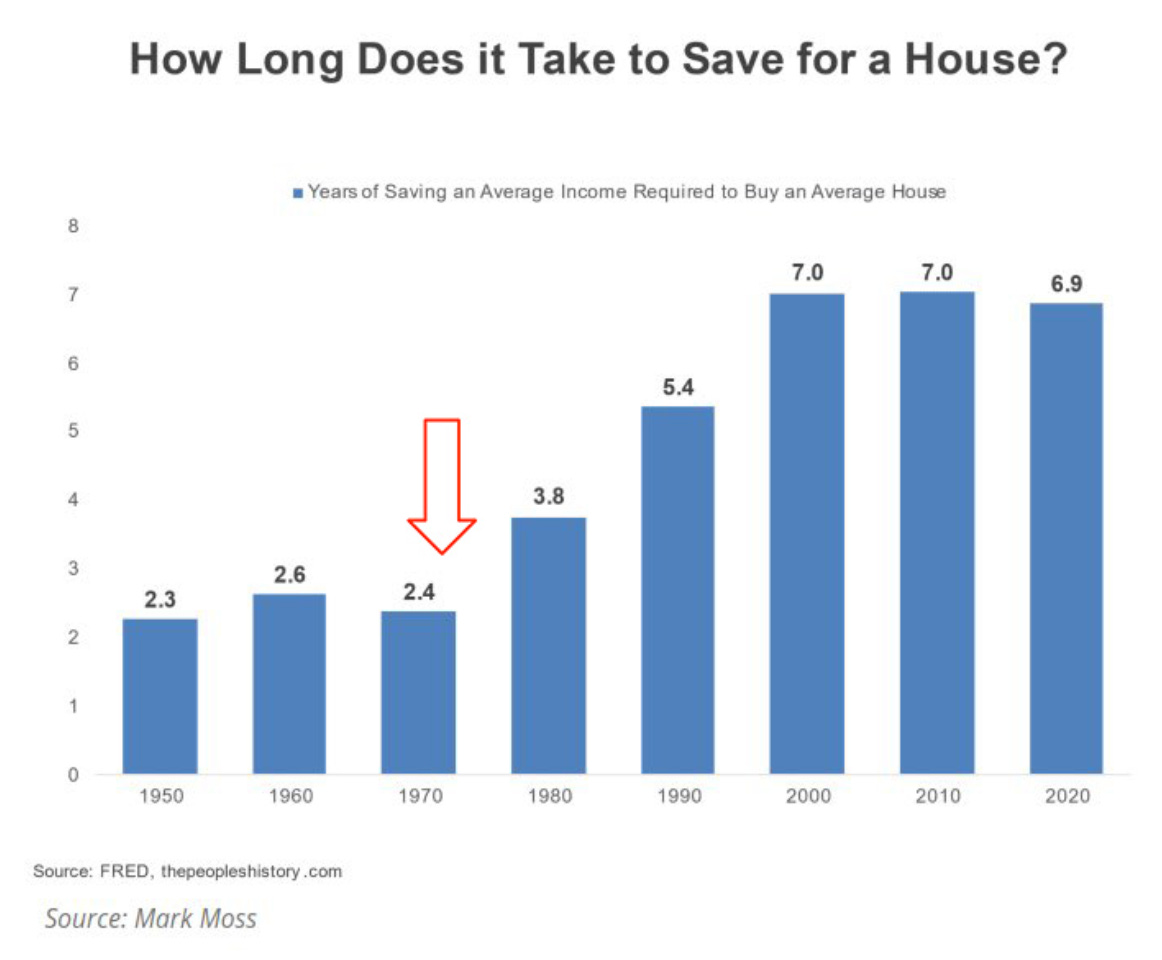

We can see how the disparity between wages and assets has only increased over time in the following charts:

The first chart shown above presents the average sales price of a house in the US alongside the average personal income, while the second chart converts this data into ratios depicting how long it took to save up for the average house on an average salary by decade.

Regardless of the format, the data paints the same sullen reality.

Since about 1971 (a significant date that deserves an entire post to discuss on it's own), the cost of the average house in comparison to the average salary has gone up exponentially.

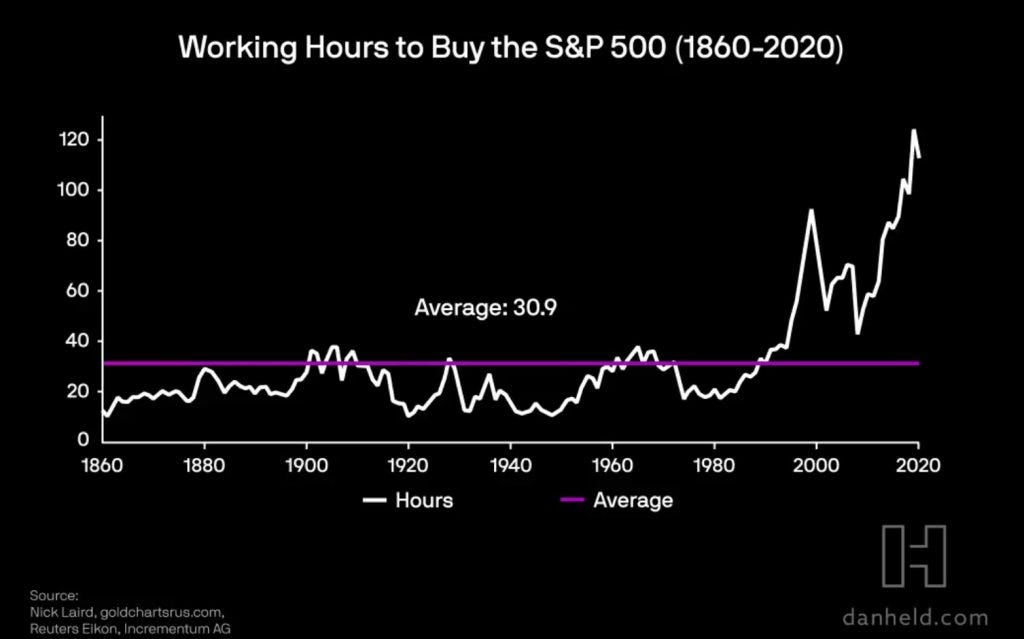

Unfortunately, we see the same disparity when analyzing stock prices from the lens of wages as well, with the average number of working hours to afford a share of the S&P 500 stock index skyrocketing in recent history.

As a final example, take the government's most recent expansion of the money supply in response to the Covid-19 pandemic.

The government flooded the economy with stimulus checks and other supportive measures that served to debase the currency by about 30% over the span of 18 months.

Real estate in highly coveted areas increased in price by 30%.

The stock market ripped higher by 30%.

Did you get a 30% raise over this period of time to compensate you?

You didn't?

Tough luck.

All of this leaves us with a single question:

If I can't save my way to financial freedom, what other options do I have?

The Risk Takers Guide To Beating Inflation

In an economy where the government has destroyed the ability of savers to retain their wealth, individuals have turned to the only other viable option: investment.

As author and economist Saifedean Ammous explains in his book The Fiat Standard, saving and investment are distinct and should ideally serve different economic functions.

According to Ammous, saving refers to stockpiling "cash balances to hedge against future uncertainty" — a strategy we already know no longer works in the modern economy.

The fundamental difference that investment brings to the table is risk.

When you invest, you do so to capitalize on the opportunity to yield a return on your money.

While some investments are more risky than others, there is no such thing as a risk-free investment.

This means that in order to preserve your purchasing power, you need to risk losing the money you have already earned.

In a healthy economy, people shouldn't need to choose between saving and investment.

But our government's constant debasement of the currency has forced all of our hands.

We've all been forced to become gamblers at the casino.

There are three primary ways to make investments that will secure and even increase your purchasing power — none are fully safe, but they're the only chance you've got:

Invest in yourself (increase your earning potential)

Invest into growth assets (multiply your value)

Invest into scarce, desirable assets (retain your purchasing power)

The first two sections will be discussing how to use investments to beat inflation, while the last section shows you how match it.

Let’s dive in.

Self Investment

Alex Hormozi nails it here.

The best way to beat inflation (not just keep up with it) is to CREATE value in excess of the value it steals from you.

The main way to do this is by investing in yourself.

Invest your time and money into the acquisition of new skills and experiences that increase your earning potential.

As your skillset continues to compound over time, you'll be able to move further and further up the wealth bracket.

Here's how this could look for someone who is just starting their journey:

Learn the skills necessary to land a job in a high paying field

Increase your skill-stack further to either secure promotions or navigate into an even more highly compensated area of expertise

Once you're skilled enough to competitively bring a product or service to market, start a business

Obviously, it's more complex than I've laid it out here.

Your progression up this very basic ladder doesn't have to linear, and it will look different for every person.

But there is one thing that is constant at every stage in this progression: risk.

With every additional step up, the amount of risk you assume grows.

But this added risk should be weighed in relation to the benefits of increased compensation should you succeed.

In other words, your continued advancement up the ladder depends entirely on your preferences in life.

You can stop whenever you feel like the reward isn't worth the risk.

There will be those who find success in the earlier steps and become comfortable with their way of life.

But there will also be others who won't stop until their quality of life matches the highest standards available.

The level of wealth you choose to generate from your contributions to society is up to you and you alone.

However, this approach can only take you so far.

The reality is no matter what level of success you're able to achieve through self investment, you'll eventually hit a wall and be stuck with the same $900 trillion dollar problem as everyone else.

A problem that spans across every economic actor on every scale: the individual, the small business, the large corporation, and even governments themselves.

How can you protect the value you've created from being inflated away?

You have two options:

Aggressive Investments: Invest in higher-risk assets that have huge potential for growth

Conservative Investments: Invest in lower-risk assets that have less potential for growth

Your portfolio may include both of these types of assets, curated to your risk tolerance.

Here's how you can think about them:

Aggressive Investments

If your goal is for your investment returns to beat the inflation rate, your portfolio should be more skewed toward assets that have high-risk associated with their performance, but have higher potential for returns.

These types of assets include:

Venture Capital & Startup Investments

Small-Cap & Emerging Market Stocks

High-Yield Bonds

Cryptocurrencies

If you choose to invest in these high-growth, high-risk assets as a vehicle to grow you wealth, here's the investing philosophy I'd recommend to you:

When it comes to generating excess returns, some of the best investors in the world all share the same belief — wealth is created with concentrated bets.

Humorously, Stanley Druckenmiller once said the best way to beat the market (and inflation) isn't being a bull or a bear: it's being a pig.

Warren Buffet has said diversification (the opposite of concentrated bets) "makes very little sense for anyone that knows what they’re doing...it is a protection against ignorance."

Lastly, Michael Saylor described diversification in a negative light as well, emphasizing that you're essentially "selling the winners to buy the losers."

The lesson here?

Learn as much as you can about the investment landscape as you can.

Strive to reach the point where you know more about a particular investment's prospects than almost anyone else.

Invest in the opportunities you've formed the highest conviction in.

If you're right, you'll massively outperform inflation and create much more wealth than you started with.

But what if you don't possess the required risk-tolerance for this strategy?

What if you're content with your returns simply matching the inflation rate?

Conservative Investments

Once you have the ability to generate substantial value, you'll find that, in a sense, you've unlocked the ability to preserve your wealth as well.

Many of the assets that actually match the true rate of monetary inflation are inaccessible to the average person.

Example: your average house in Kansas isn't as scarce or desirable as a house in the Hamptons, so the rate of its appreciation will not keep up with the latter.

Now that you've acquired an abundance of financial resources, you've unlocked an entirely new tier of assets you can invest in to shield your wealth from inflation, including:

Coveted Real Estate (Commercial real estate, beachfront property)

Business Equity (Ownership in private & public companies)

Luxury Goods & Collectibles (High-end vehicles, jewelry, art, rare baseball cards)

Normally, in a world without rampant inflation, the value of these assets would be determined solely by supply and demand, market conditions, and their utility to the holder.

But the relentless expansion of the money supply has added a MASSIVE value premium to these assets because of their unique ability to keep pace with the inflation rate due to their scarcity and desirability.

This has given rise to these assets being used as a Frankenstein investment vehicle where the assets preserve traits from both a savings account and an investment at the same time.

These assets can retain your purchasing power into the future like a savings account ideally should, albeit imperfectly, as they also suffer from the inherent risk that comes with any form of investment.

As the value of the currency plummets, we've seen countless wealthy investors subscribe to this investing philosophy, resulting in nothing short of a stampede into hard assets within the categories listed above.

As a result, the ownership of hard assets is HIGHLY skewed toward the rich.

The wealthiest 10% of Americans own 93% of all stocks.

Presidential candidate RFK Jr. warns that by 2030, major corporations could own 60% of all homes.

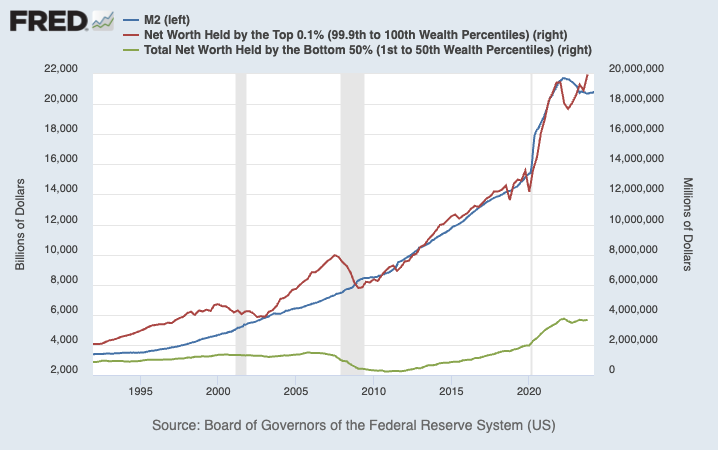

In the following chart, you can see exactly how this investment thesis has played out:

Using the M2 metric as our proxy for the total amount of money circulating in the economy, we can see that the wealth of the 0.1% has perfectly tracked the expansion of the money supply.

Needless to say, the wealth of the bottom 50% of the population hasn't kept pace at all.

This stark contrast in outcomes is rooted in a simple reality:

The rich own the scarce and desirable assets that the poor do not.

But all hope isn’t lost.

"Two hundred years ago, before the advent of capitalism, a man's social status was fixed from the beginning to the end of his life; he inherited it from his ancestors, and it never changed." — Ludwig von Mises

Despite the situation of the poor and middle class becoming more bleak by the day, the system of capitalism provides a way out.

While class mobility in the United States has been declining in recent years because of inflation, there is still an abundance of opportunity to build the life you want to lead.

I’ll leave you with this advice:

Take the risks you need to take to build the life you want

Store the wealth you acquire in assets that will hold their value across time

Pass those assets down to your children, and educate them to repeat the process

Until next time.

— Landon